Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

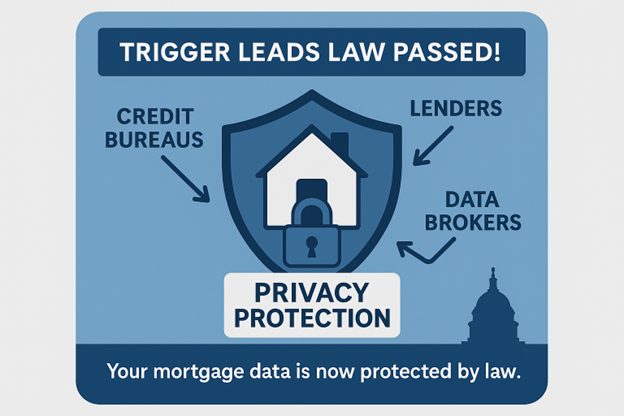

Major Win for Homebuyer Privacy: Understanding the New Trigger Leads Law

As your trusted real estate professional, I want to share some important news that directly affects your privacy and peace of mind when applying for a mortgage. A significant new law has been enacted that addresses a practice many homebuyers didn’t even know was happening behind the scenes.

What Are Trigger Leads?

Before diving into the new legislation, let’s explain what trigger leads are. When you apply for a mortgage loan, credit reporting agencies have historically been able to sell your personal financial information to competing lenders and mortgage brokers without your knowledge or consent. This practice, known as “trigger leads,” occurs immediately after you submit a mortgage application and the lender pulls your credit report.

The result? You’ve likely experienced it yourself – a flood of phone calls, emails, and text messages from other lenders trying to steal business from your chosen mortgage professional. Many homebuyers mistakenly believe their real estate agent or original lender sold their information, when in reality, it was credit bureaus monetizing their data without permission.

The New Law: Homebuyers Privacy Protection Act

In August 2025, the Senate unanimously passed the Homebuyers Privacy Protection Act of 2025, which was subsequently signed into law by President Trump. This bipartisan legislation represents years of advocacy from the National Association of Realtors, banking organizations, and consumer protection groups who recognized the need to address these abusive practices.

The new law prohibits consumer reporting agencies from furnishing trigger leads unless an individual chooses to opt-in, and even then, only certain approved groups will be notified that someone is seeking a new mortgage.

Key Protections Under the New Law

The legislation establishes several important safeguards for homebuyers:

Consent Requirement: Credit bureaus can only share trigger leads if the borrower has given their explicit consent. No more surprise solicitations from unknown lenders.

Limited Recipients: Data can only go to your current lender, loan servicer, or a company you already have an existing relationship with. This prevents random lenders from accessing your information.

Firm Offer Requirement: Under the new framework, consumer reporting agencies may release a mortgage-related trigger lead only if the recipient makes a firm offer of credit or insurance and qualifies under narrow criteria.

Implementation Timeline: The new restrictions take effect six months after the law was signed, giving the industry time to adjust their practices while providing immediate relief to consumers.

What This Means for You as a Homebuyer

This legislation represents a major victory for consumer privacy and will significantly improve your homebuying experience in several ways:

Reduced Harassment: You’ll no longer be bombarded with unwanted calls, emails, and texts from competing lenders after applying for a mortgage. This allows you to focus on working with your chosen mortgage professional without distractions.

Protected Privacy: Your personal financial information will remain confidential between you and your selected lender, unless you specifically choose to share it with others.

Clearer Communication: You’ll have a better understanding of who has access to your information and why they’re contacting you, eliminating confusion about whether your agent or lender inappropriately shared your data.

Better Service Experience: With fewer interruptions from competing lenders, you can maintain stronger relationships with your chosen mortgage professional, leading to better service and communication throughout the loan process.

Industry Support and Bipartisan Effort

The success of this legislation demonstrates remarkable bipartisan cooperation. The bill was championed by Senators Bill Hagerty (R-TN) and Jack Reed (D-RI), along with Representatives John Rose (R-TN) and Ritchie Torres (D-NY). Chairman French Hill of the House Financial Services Committee praised the law as protecting homebuyers’ personal financial information while encouraging competition in the mortgage market.

Multiple industry organizations supported the legislation, including the National Association of Realtors, American Bankers Association, and various consumer protection groups. This broad coalition recognized that addressing trigger leads would benefit both consumers and legitimate mortgage professionals who compete based on service quality rather than aggressive marketing tactics.

Looking Ahead

As your real estate agent, I’m committed to staying informed about changes that affect your homebuying experience. The National Association of Realtors will continue monitoring the implementation of this law to ensure both real estate professionals and consumers are protected.

This new legislation represents a significant step forward in protecting consumer privacy while maintaining healthy competition in the mortgage marketplace. When you’re ready to begin your homebuying journey, you can now do so with greater confidence that your personal information will be handled responsibly.

The mortgage application process should be about finding the right loan for your needs, not about defending yourself against unwanted solicitations. With the Homebuyers Privacy Protection Act now in effect, that’s exactly what you can expect – a more streamlined, privacy-focused experience that puts your interests first.

If you have questions about how this new law affects your specific situation or need guidance navigating the mortgage application process, don’t hesitate to reach out. As your trusted real estate professional, I’m here to help you understand these changes and ensure your homebuying experience is as smooth and stress-free as possible.